CSRD Timeline – Stay ahead of reporting schedule

CSRD timeline outlines the phased implementation of the Corporate Sustainability Reporting Directive, starting from 2024, with the first set of companies required to apply the new rules for the 2024 financial year, leading to reports published in 2025.

CSRD (Corporate Sustainability Reporting Directive) came into force 1.1.2023, and became applicable 1.1.2024. CSRD will strengthen and standardize the rules for how companies in EU are required to disclose information on their impact on people and the planet.

CSRD Timeline in 2025

From FY 2025, large listed and private companies and consolidated groups that meet at least two of the following criteria: more than 250 employees, balance sheet of more than 25 million euros, or more than 50 million euros in turnover.

To prepare for reporting in 2025:

- Prepare reporting systems. Ensure you have clear Key Performance Indicators (KPI’s), goals and a plan in place.

- Gather data throughout the year for 2025 reporting and review it with your controller.

Note, if your company is subjected to NFRD you are required to report on 2024 data in 2025.

In FY 2025, review your reporting activities and systems to establish or improve your reporting in 2026. If you are not required to report under CSRD in 2025, note that you may receive information requests from your customers requiring information on their supply chain.

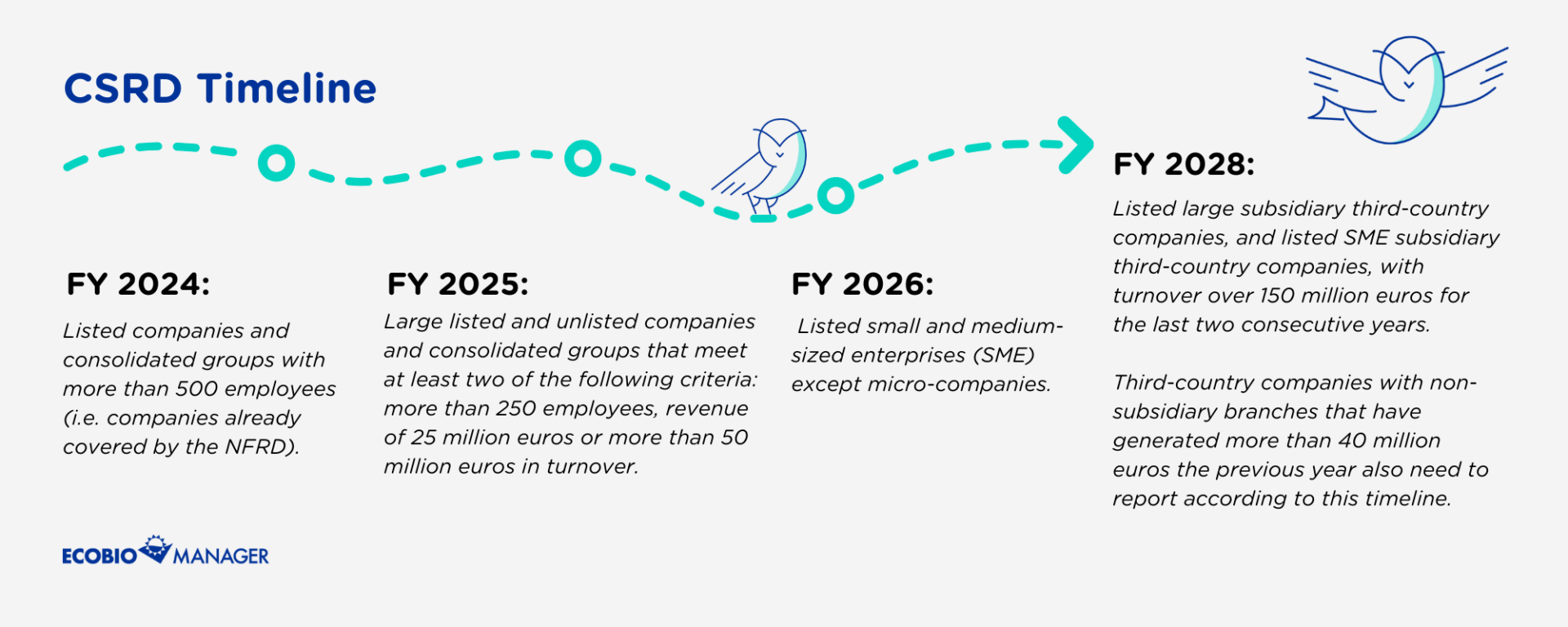

CSRD Timeline and Impact on companies from 2024 to 2028

The CSRD applies to companies in the following order (according to Article 5 in CSRD):

- from financial year (FY) 2024, listed companies and consolidated groups with more than 500 employees (i.e. companies already covered by the NFRD);

- from FY 2025, large listed and private companies and consolidated groups that meet at least two of the following criteria: more than 250 employees, balance sheet of 25 million euros, or more than 50 million euros in turnover;

- from FY 2026, listed small and medium sized enterprises (SME) except micro-companies;

- From FY 2028, listed large subsidiary third-country companies, and listed SME subsidiary third-country companies, with turnover over 150 million euros for the last two consecutive years. Third-country companies with non-subsidiary branches that have generated more than 40 million euro the previous year also need to report according to this timeline. Reports are required on a group level, or individual level for branches without an applicable group level.

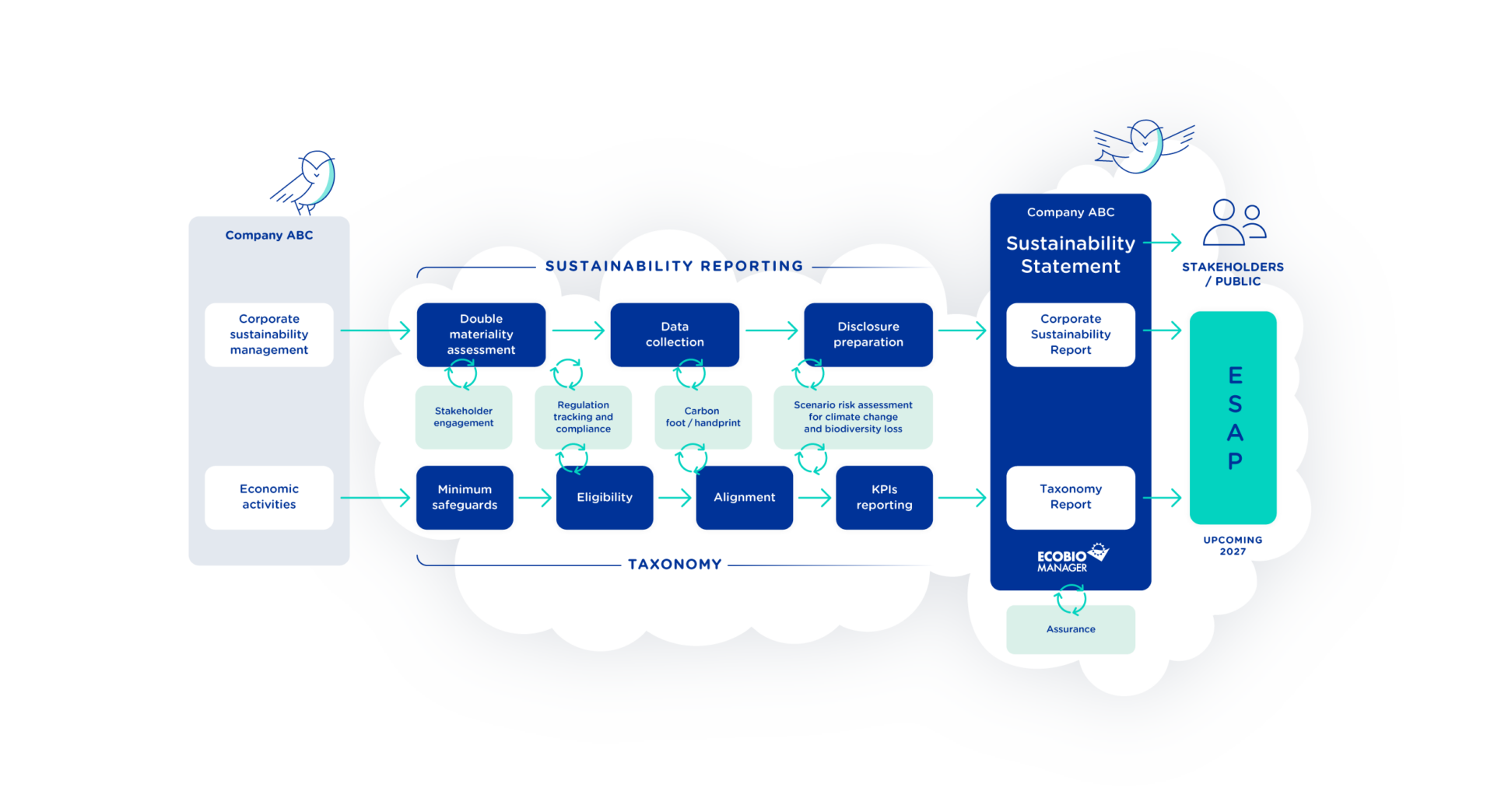

CSRD data collection and reporting

Under the CSRD, companies are required to assess their sustainability matters following the double materiality principle. Conducting a double materiality assessment means that companies assess both the impact of a company on society and the environment (impact materiality) and the impact society and environment has on the company (financial materiality).

The decision of which sustainability topics and data a company needs to collect and report on depends on that company’s most important material topics.

Ecobio Manager CSRD solution helps you with data collection under CSRD requirements. Bid farewell to manual data entry. Our solution seamlessly integrates assessment results into your data collection system, saving you valuable time and effort. Read more here.