EU Taxonomy Minimum Safeguards – Everything You Should Know

EU Taxonomy Minimum Safeguards ensure that companies whose economic activities can be defined as environmentally sustainable under EU Taxonomy adhere to good practices, such as respecting human rights and fair treatment of the workforce.

The EU Taxonomy is a classification system that defines activities that are considered environmentally sustainable. It creates a common language that companies, investors, and governments can use to express opinions or facts about sustainable activities clearly and consistently.

For economic activity to be classified as environmentally sustainable, it must fulfil the following conditions:

- substantially contributes to one or more environmental objectives

- does not significantly harm (DNSH) any other environmental objective

- complies with minimum safeguards based on human rights standards

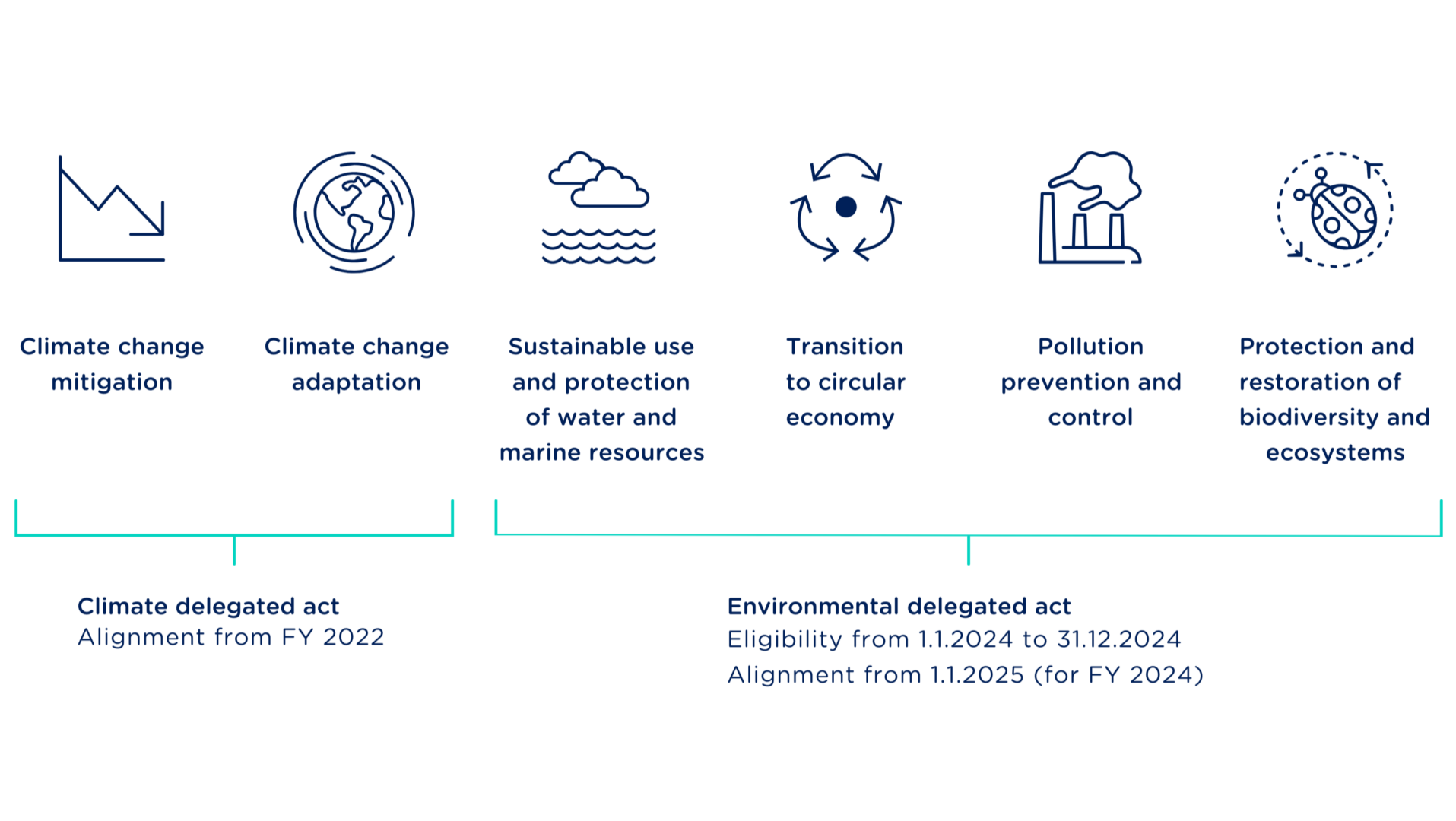

What are the six criteria for EU Taxonomy?

The six EU Taxonomy criteria refer to 6 environmental objectives under which activities will be defined.

- climate change mitigation

- climate change adaptation

- sustainable use and protection of water and marine resources

- transition to circular economy

- pollution prevention and control

- protection and restoration of biodiversity and ecosystems.

What are the minimum safeguards for EU taxonomy?

The minimum safeguards require companies to have due diligence processes in place that cover the following topics: human rights (including labour and consumer rights), taxation, fair competition, bribery, bribe solicitation, and extortion.

Companies whose economic activities are to be considered as taxonomy aligned have to align with the standards for responsible business conduct mentioned in:

• the OECD Guidelines for Multinational Enterprises,

• the UN Guiding Principles on Business and Human Rights,

• the ILO Declaration on the Fundamental Principles and Rights at Work,

• the eight fundamental conventions of the ILO on human and labour rights,

• the International Bill of Human Rights.

What is Article 18 of the EU taxonomy regulation?

Article 18 in the EU Taxonomy regulation (EU 2020/852) establishes the use of minimum safeguards. The purpose of Article 18 is to prevent green investments from being labelled and regarded as ‘sustainable’ when they involve negative impacts on human rights or are linked to non-compliance.

The Platform on Sustainable Finance on Safeguards (Final report on minimum safeguards) provided further recommendations on what it means to comply with minimum social safeguards or not comply with them.

Compliance with the minimum social safeguards

The labour rights covered by the ILO fundamental conventions are signed and implemented by many countries and should be implemented in national legislation. Thus, prohibition of child and forced labour, tax fraud, corruption and bribery, and unfair competition should already be mandatory for companies. But compliance need to be ensured, monitored and disclosed.

In addition to compliance with labour, taxation, anti-corruption and fair competition legislation, companies need to establish adequate due diligence processes on human rights issues that comply with the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights Following the OECD guidelines, a due diligence process embeds responsible business conduct in company polices and management systems, includes a risk assessment of impacts associated with company operations, products or services, implements measures to mitigate risks and impacts, tracks and monitors the implementation and results and communicates results. An important step is also to ensure that the process is continuously improved.

Power of digitalisation for compliant CSRD Reporting

EU Taxonomy and CSRD reporting promotes a digital approach from the beginning, rendering manual efforts time-consuming, inefficient and resource-draining. Compliance with CSRD will require electronically tagged information and submission to the ESAP via the National Contact Point from January 2028. Achieving CSRD requirements without specialised software will be increasingly difficult due to the shear amount of data and information that needs to be collected. Enter Ecobio Manager: Your solution for seamless electronic tagging and ESAP delivery.

Streamline CSRD Reporting with Ecobio Manager

Ecobio Manager is a comprehensive solution for CSRD sustainability reporting, encompassing double materiality assessment, data collection, taxonomy classification and KPI reporting, sustainability statement preparation, assurance, and streamlined delivery of electronically tagged information for publication. Designed by sustainability experts, Ecobio Manager ensures compliance with CSRD, ESRS standards, and EU Taxonomy regulation, streamlining the reporting process.