CSRD Framework and Legal Background – What is the new CSRD Regulation?

The CSRD framework is a complex collection of reporting requirements on sustainability information. In this article, we’ll outline the legal background and the requirements of EU’s new directive.

Corporate sustainability reporting directive (CSRD) is part of the EU’s Green Development Agenda for the business sector. To achieve sustainability goals, the EU has implemented the Corporate Sustainability Reporting Directive (CSRD, EU 2022/2464) and Taxonomy Regulation (EU 2020/852). These two legislative texts define a new digital sustainability reporting framework for EU companies.

Corporate Sustainability Reporting Directive – CSRD framework and legal requirements

The Corporate Sustainability Reporting Directive is commonly referred to as a framework. However, in correct terms the CSRD is not one. It is a directive issued by the European Council, complemented by the ESRS reporting standards. These two are not just a loose set of best practices; rather, they are rules for sustainability reporting that companies must comply with. While the CSRD allows for some flexibility through the ESRS transitional provisions, it remains a legally binding.

The Corporate Sustainability Reporting Directive (CSRD), effective January 2023, is an amending legislative act affecting existing directives such as the Accounting Directive (2013/34/EU), the Transparency Directive (2004/109/EC), and the Audit Directive (2006/43/EC). The CSRD effectively replaces the previous non-financial reporting directive (NFRD, 2014/95/EU) and defines mandatory sustainability reporting for a wider collection of companies and other entities within EU. Its provisions will require companies to disclose environmental, social and governance information, including information across value chains.

CSRD is one of the actions implemented under the EU Green Deal and the sustainable finance action plan and aims to foster transparency by strengthening sustainability reporting and accounting. Through this goal, the CSRD helps investors identify companies engaged in sustainable activities.

CSRD legal requirements in a nutshell

| Reporting standards | Digital reporting | Assurance – digitally |

|---|---|---|

| Information must be reported according to the European Sustainability Reporting Standards (ESRS, (EU) 2023/2772) This ensures data quality and consistency. | The information in the sustainability statement must be available in a digital, machine-readable format. Data will be transferred to the European Single Access Point (ESAP) database via national contact points. | The sustainability information must be verified by an independent party under limited assurance. Information must be reliable, well-documented, and traceable. |

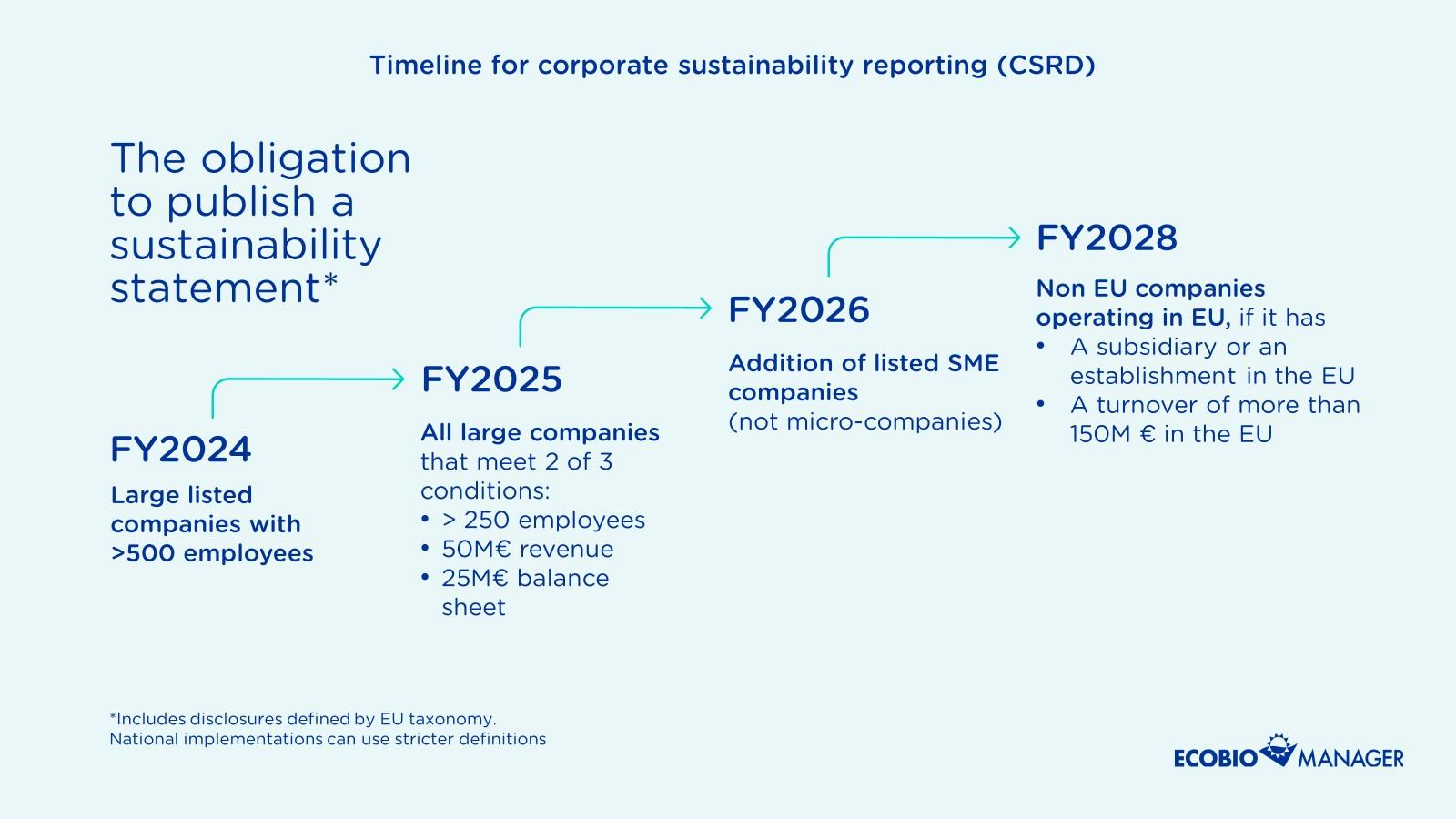

Who needs to comply with CSRD?

The legislative obligations for companies will come into force gradually over four years, starting with large, listed companies with over 500 employees needing to report on information from the financial year 2024. All large companies that meet 2 of 3 conditions must comply from 2025: more than 250 employees, 50M€ revenue or 25M€ balance sheet. From 2026, listed SME companies will be added.

Non-EU -companies that operate in the EU must comply with the reporting requirements from 2028 if they have a subsidiary or an establishment in the EU and a total turnover of more than 150M€ within the EU. Small businesses are, in practice, asked to provide similar information through the supply chain.

Taxonomy Regulation and Related Delegated Acts – The financial side of the CSRD legal framework

The EU Taxonomy Regulation connects financial performance to sustainability reporting. The EU Taxonomy is the European Union’s means for companies to implement the EU Green Deal goal to transition to a low-carbon and resource-efficient future from a financial perspective. It applies to both financial and non-financial sectors.

The EU Taxonomy requires companies to classify their environmentally sustainable activities and investments and report related economic key performance indicators (KPIs) annually. The classification requirements are defined as Technical Screening Criteria published as delegated regulations, the climate delegated act (EU) 2021/2139 and the environmental delegated act (EU) 2023/2486, while the reporting requirements are defined in a separate delegated regulation.The large amount of defined activities, their related technical screening criteria and associated legislation require good management procedures.

Although the EU Taxonomy reporting requirements are separate from the CSRD, the CSRD requires that companies include their taxonomy report as part of the sustainability statement prepared through ESRS.

EFRAG and ESRS

The European Commission mandated The European Financial Reporting Advisory Group (EFRAG) to develop, define, and interpret the reporting obligations in detail as a European sustainability reporting standard (ESRS). While CSRD directs legislation development of EU member states, the ESRS requirements apply directly to companies.

EFRAG serves the European public interest in financial and sustainability reporting. Regarding CSRD, EFRAG provide technical advice to the European Commission by preparing draft sustainability standards and draft amendments to those. Regarding financial reporting, EFRAG influence the development of IFRS standards from a European perspective. The ESRS standards for large companies are already ready and published ((EU) 2023/2772), while EFRAG is still preparing the draft standards for listed small and medium-sized enterprises (SMEs) and for voluntary SME reporting. In addition, first drafts of the upcoming sector standards are expected during this year.

What happens if a company does not comply with CSRD legal requirements?

The CSRD itself does not define sanctions for non-compliance with the sustainability reporting requirements and the Accounting Directive (2013/34/EU) leave the provisioning of sanctions up to each member state. It is therefore essential to check the national implementation of the CSRD and reporting requirements for information on possible sanctions for non-compliance with reporting requirements.

However, non-compliance with CSRD may impact for example access to funds and investors through other routes in cases where investment decisions are based on sustainability performance and the company’s capability to manage risks to the business that arise from sustainability issues. When established in 2027, the ESAP database will enable investors to easily access sustainability data and compare companies, leading investments and the economy to a greener future.

Power of digitalisation for compliant CSRD Reporting

The complexity of CSRD reporting promotes a digital approach from the beginning, rendering manual efforts time consuming, inefficient and resource draining. Compliance with CSRD requires the sustainability information to be electronically tagged and submitted to the European Single Access Point from January 2028. Achieving CSRD requirements without specialised software will be increasingly difficult due to the shear amount of data and information that needs to be collected. Enter Ecobio Manager: Your solution for seamless electronic tagging and ESAP delivery.

Streamline CSRD Reporting with Ecobio Manager

Ecobio Manager is a comprehensive solution for CSRD sustainability reporting, encompassing double materiality assessment, data collection, taxonomy classification and KPI reporting, sustainability statement preparation, assurance, and streamlined delivery of electronically tagged information for publication. Designed by sustainability experts, Ecobio Manager ensures compliance with the CSRD, ESRS standards and the EU Taxonomy regulation, streamlining the reporting process.

CSRD Sustainability reporting software for cost-savings and compliance

Smooth workflow for your team – from double materiality assessment to sustainability statement.