Why is Stakeholder Engagement Crucial in CSRD Reporting?

Stakeholder engagement is crucial for a successful sustainability reporting (CSRD) process. The foundation of the CSRD reporting process is the Double Materiality Assessment, for which the European Sustainability Reporting Standards (ESRS) requires companies to consider stakeholder’s views and impacts.

Stakeholder Engagement in the CSRD Double Materiality Assessment

The sustainability reporting process starts with a Double Materiality Assessment. The company must identify their material impacts, risks and opportunities that arise from sustainability matters, those defined in the ESRS and others. Identification of impacts addresses how the company’s operations and activities affect the environment and people, identification of risks and opportunities addresses how environmental and social matters affect the company.

Companies can assess double materiality using either a top-down or bottom-up approach

- A top-down approach identifies the impacts, risks and opportunities arising from sustainability matters at the topic, sub-topic or sub-sub-topic level.

- A bottom-up approach identifies potential material sustainability matters based on impacts, risks and opportunities that are identified for example through existing internal risk management or due diligence processes.

The Sustainability Statement is intended for the Stakeholders. This is why stakeholder engagement from the beginning is so important

The sustainability statement is intended to meet the information needs of stakeholders. In ESRS, stakeholders are divided into two groups:

Affected stakeholders are individuals or groups whose interests are affected or could be affected, positively or negatively, by the company’s activities and its direct and indirect business relationships across its value chain. This includes the company’s value chain but can also include other stakeholder groups such as local communities or silent stakeholders such as nature;

Users of sustainability statements include investors, lenders or other creditors, trade unions, NGO’s, or similar entities that use the information provided in sustainability statements, for example, for decision-making. Many stakeholders belong to both groups.

Regardless of the approach followed for conducting the double materiality assessment, it is key to identify which sustainability matters are material, based on material impacts, risks and opportunities. Information from affected stakeholders typically informs the identification of impacts on sustainability matters, while information from users of sustainability statements may be more important for identifying financial risks and opportunities. Given that a topic is a material, the reason for this can usually be found in the crossroad between the sub-topic or sub-sub-topic and the value chain (affected stakeholder).

Being able to assess stakeholder information requires good communication with the relevant parties, which means that the double materiality assessment is further founded on a solid stakeholder engagement process that covers, for example, customers, suppliers, investors, employees and authorities, to mention some.

How can stakeholder dialogue affect double materiality assessment?

Companies should identify their key affected stakeholders by analysing existing initiatives and mapping the affected stakeholders across their activities and business relationships. When conducting the Double Materiality Assessment, companies should take the views of and impacts on their affected stakeholders into account. This can be done for example by gathering feedback through surveys or interviews.

Stakeholders matter! Stakeholder engagement and feedback are crucial for building a complete picture of the true scale of how the company affects its surroundings.

In addition, gathering a broad base of stakeholder feedback can inspire and promote productive conversations about sustainability matters.

Power of digitalisation for compliant CSRD Reporting

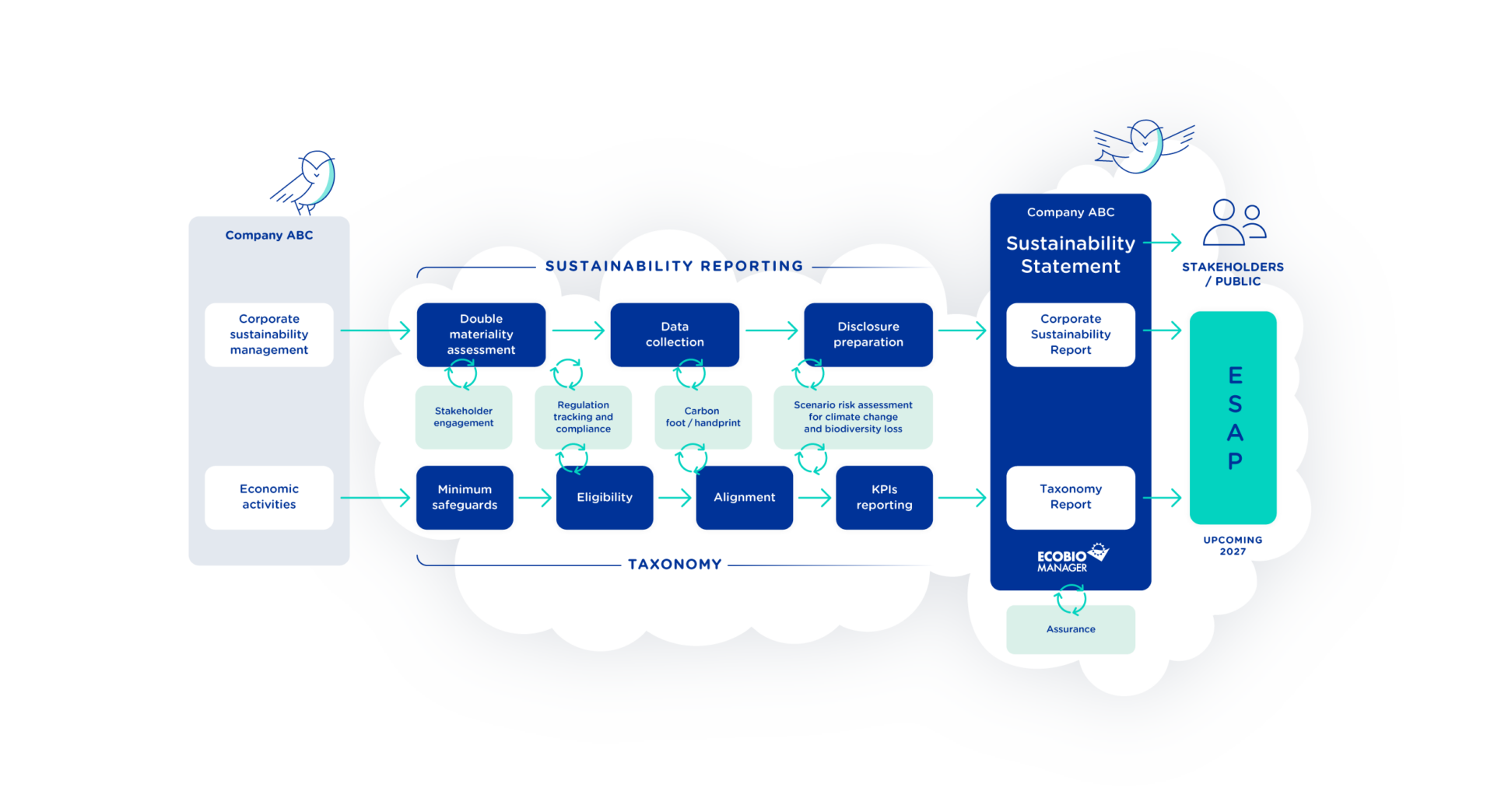

CSRD reporting promotes a digital approach from the beginning, rendering manual efforts time-consuming, inefficient and resource-draining. Compliance with CSRD will require electronically tagged information and submission to the ESAP via the National Contact Point from January 2028. Achieving CSRD requirements without specialised software will be increasingly difficult due to the shear amount of data and information that needs to be collected. Enter Ecobio Manager: Your solution for seamless electronic tagging and ESAP delivery.

Streamline CSRD Reporting with Ecobio Manager

Ecobio Manager is a comprehensive solution for CSRD sustainability reporting, encompassing double materiality assessment, data collection, taxonomy classification and KPI reporting, sustainability statement preparation, assurance, and streamlined delivery of electronically tagged information for publication. Designed by sustainability experts, Ecobio Manager ensures compliance with CSRD, ESRS standards, and EU Taxonomy regulation, streamlining the reporting process.